Investment returns were surprisingly strong in the first half of this year despite a wall of worries. Dr Shane Oliver reminds us that markets can change direction quickly and that there’s plenty of risk still lurking. In his latest insight he highlights seven charts that investors should keep an eye on, from tariffs and business conditions to earnings and the US dollar. Below is our summary of those charts and what they mean for your portfolio.

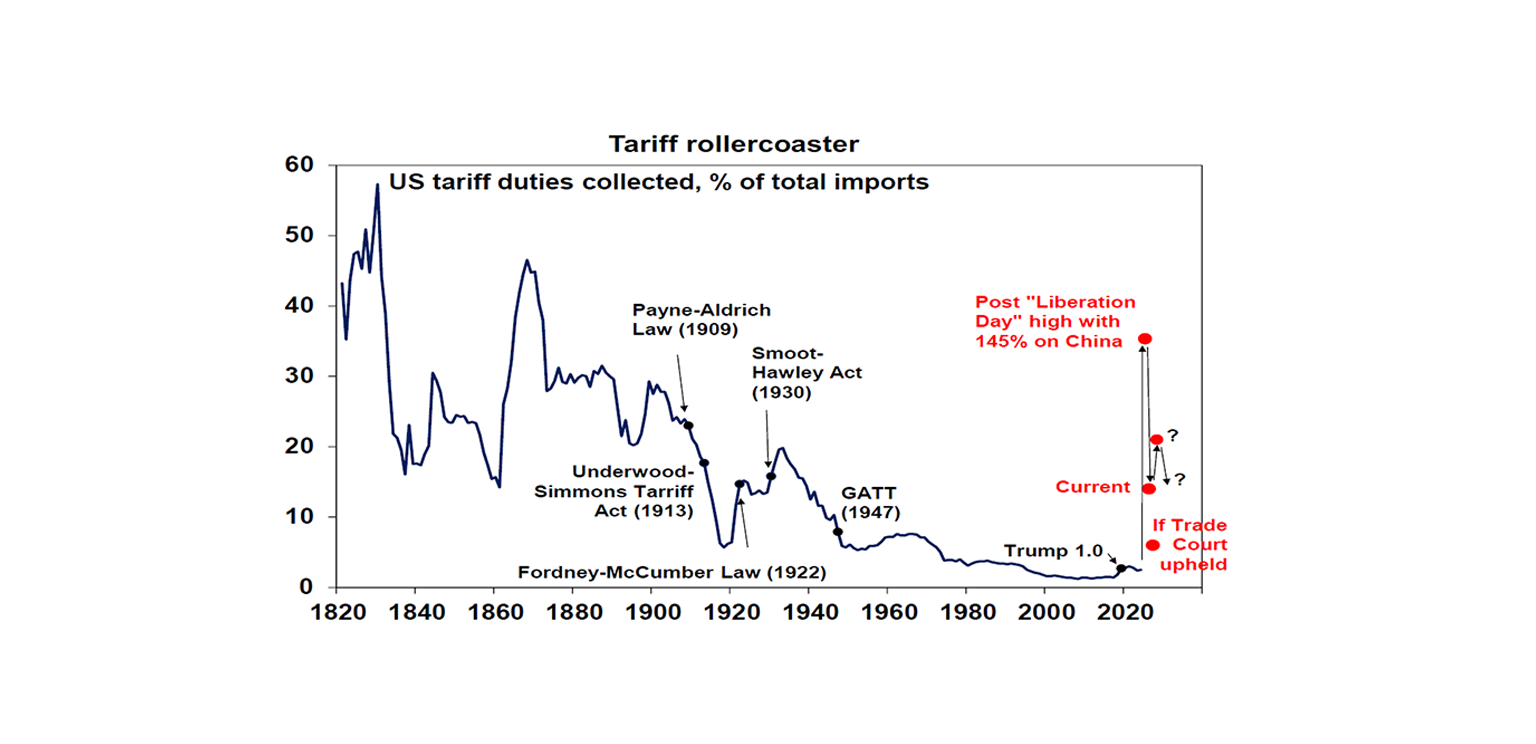

1. The US tariff rollercoaster

The escalation and de‑escalation of US tariffs have been a major driver of market swings this year. Average US tariffs jumped from around 3 % to more than 30 % in early April after “Liberation Day” announcements, then eased back during 90‑day negotiating pauses. With new rounds of tariffs pending on countries from Japan to Myanmar, the average could settle around 20 %. For Australia, which sends less than 5 % of its goods exports to the US, the direct impact is minor; the bigger risk is that widespread tariffs slow global growth and trigger share‑market corrections.

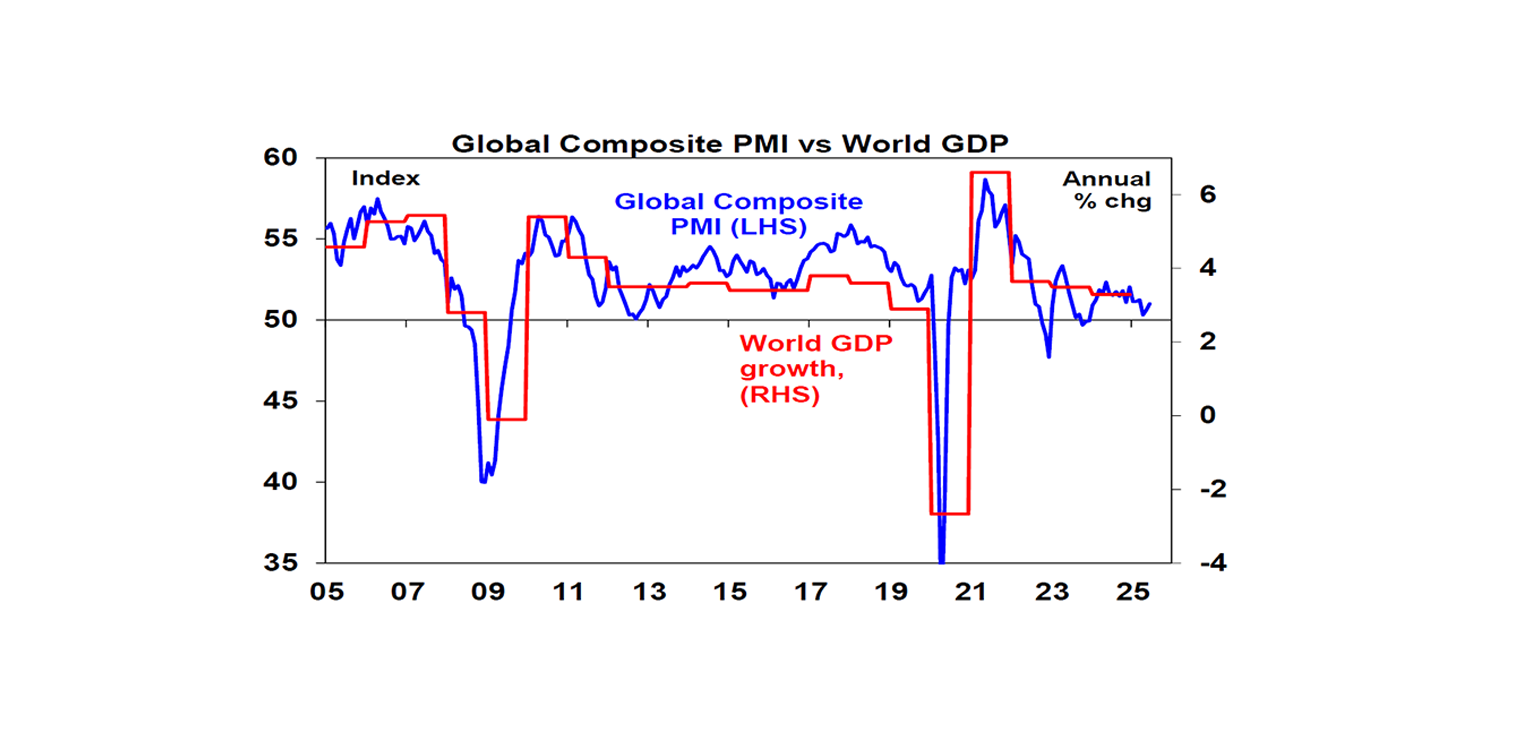

2. Global business conditions PMIs

Purchasing managers’ indices (PMIs) are a timely gauge of business activity and provide an early warning of economic turning points. Dr Oliver notes that PMIs have slowed but are not collapsing. If major economies avoid recession, any fall in shares should be short‑lived. However, if tariffs do more damage than expected, a deeper slump in PMIs would flag trouble ahead.

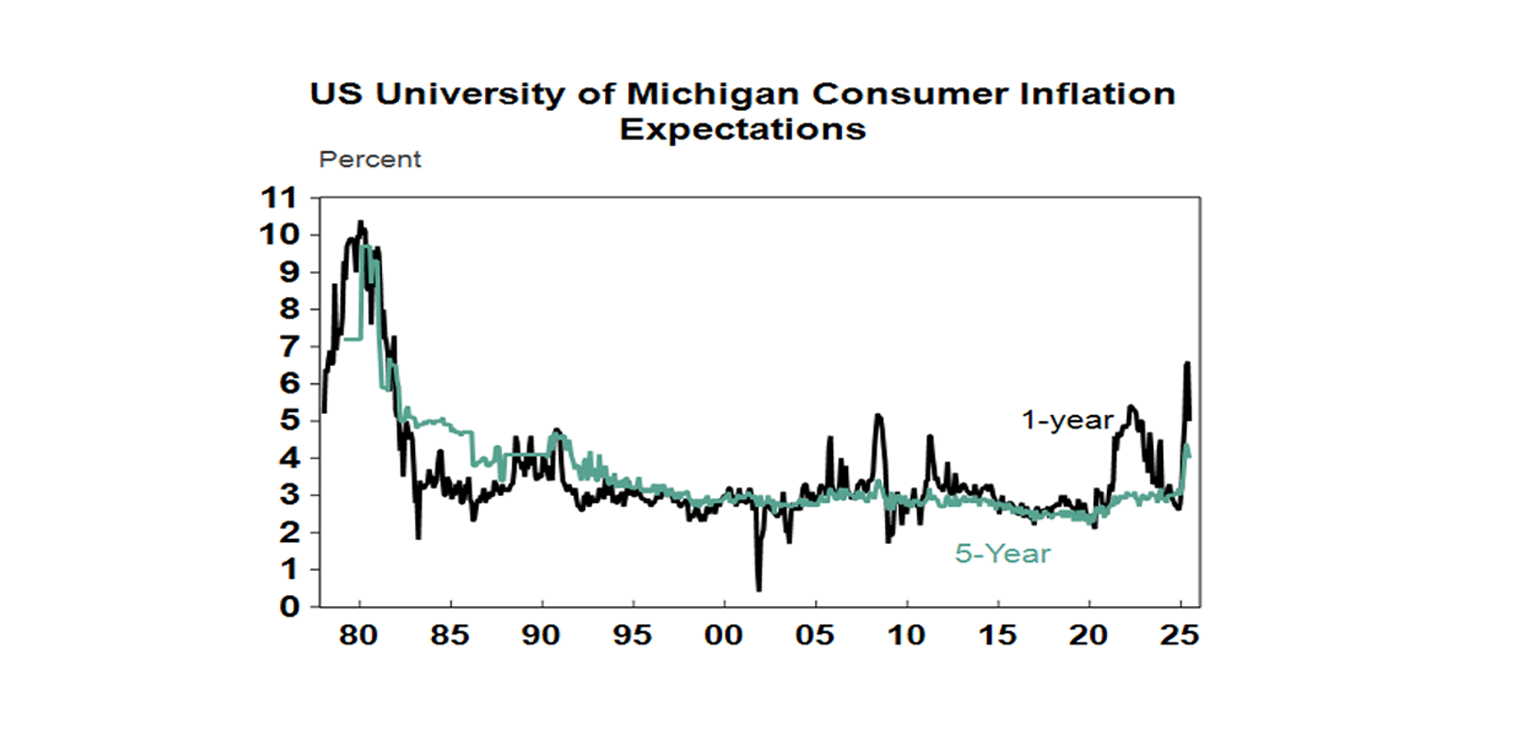

3. Longer‑term inflation expectations

The post‑pandemic inflation surge fortunately didn’t unanchor medium‑term inflation expectations, which stayed low and allowed central banks to focus on bringing inflation down. This year, however, tariff rhetoric has nudged some measures of US consumer inflation expectations higher. Elevated expectations could keep the US Federal Reserve on hold longer and slow the pace of rate cuts. Encouragingly, this is primarily a US phenomenon; inflation expectations remain well behaved elsewhere, including in Australia.

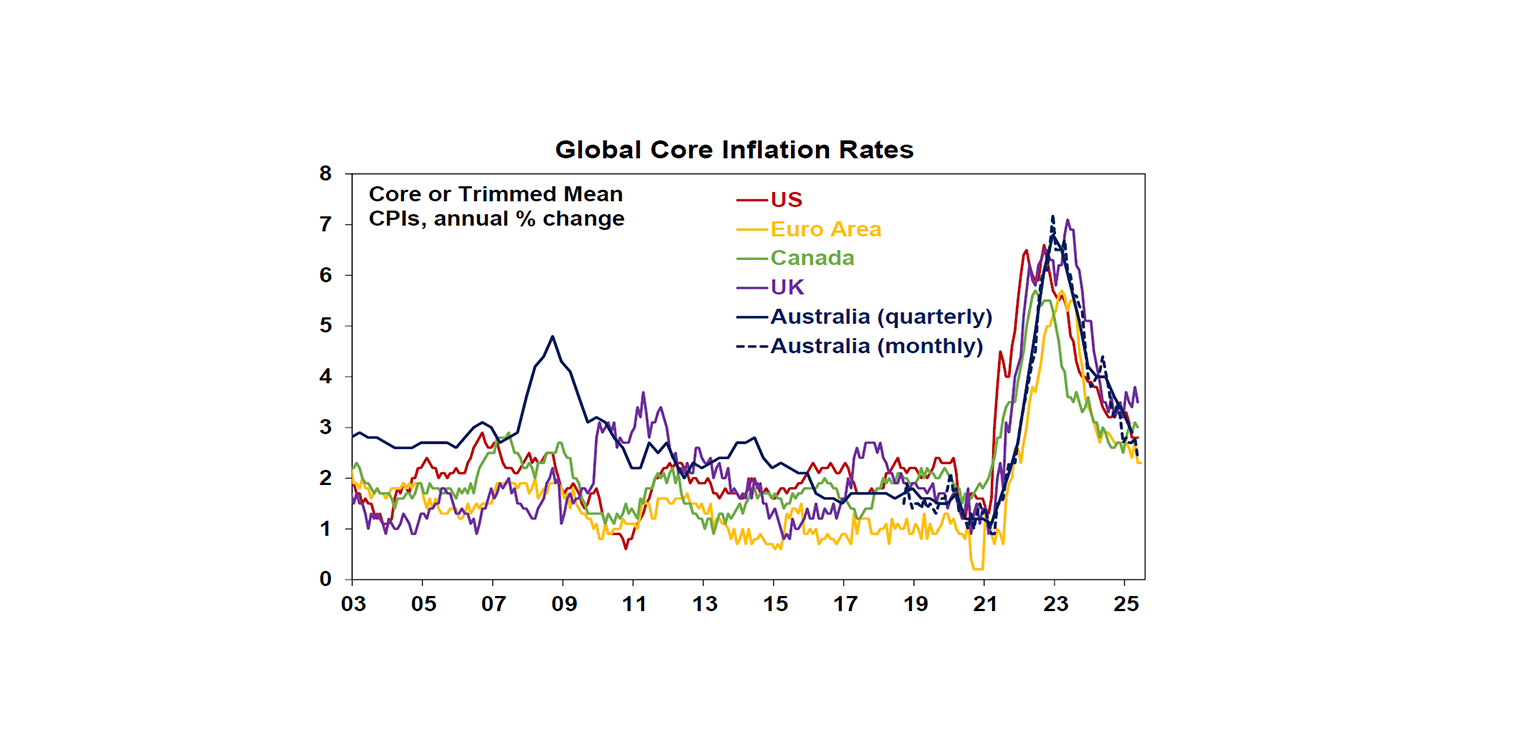

4. Inflation – and what it means for interest rates

Central banks need inflation to settle near their targets to justify further rate cuts. Dr Oliver points out that underlying inflation is already within the Reserve Bank of Australia’s 2–3 % band, and he expects another four quarter‑point reductions over the next year or so, taking the cash rate to around 2.85 %. In other parts of the world, tariffs could give US inflation a one‑off bump but are unlikely to derail the broader disinflation trend.

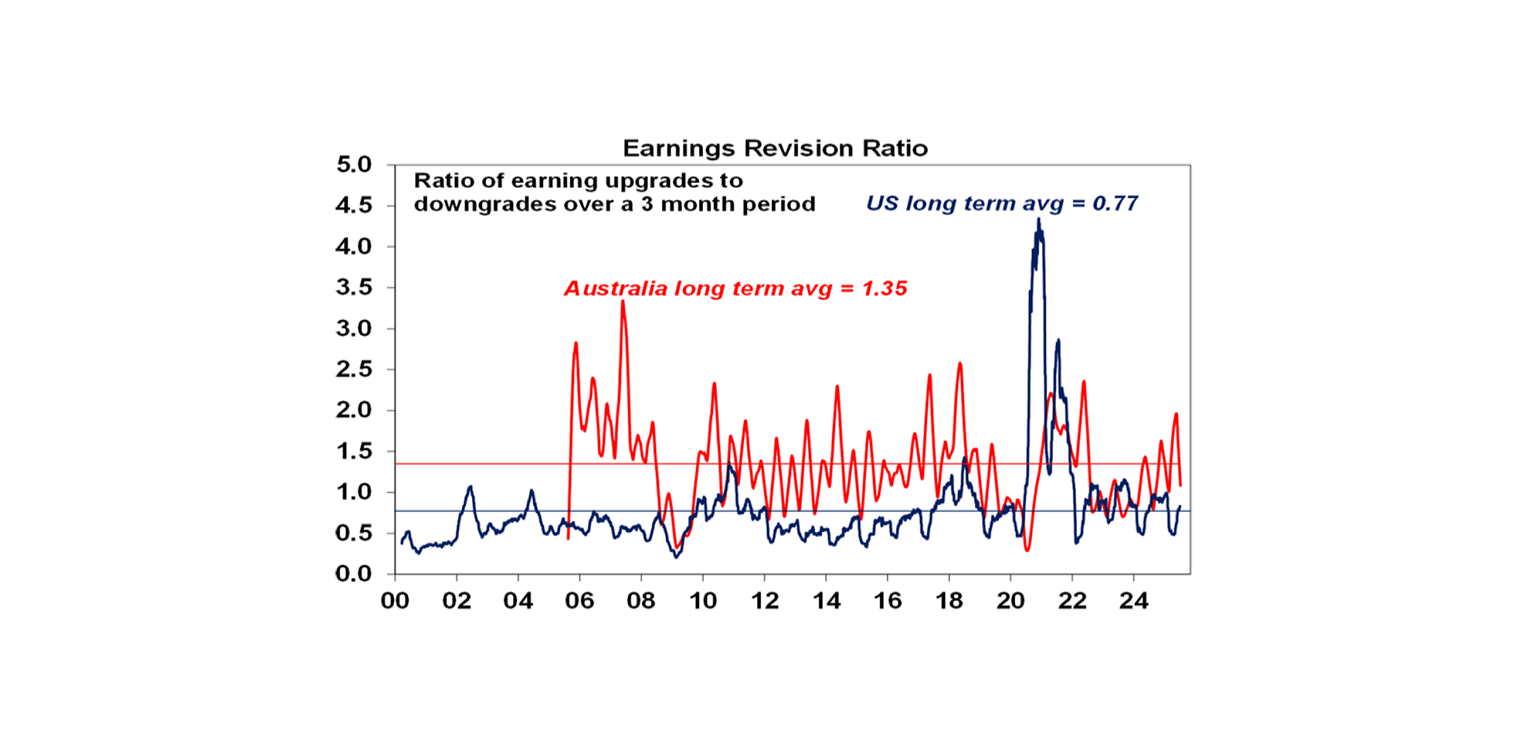

5. Company profit outlook

Consensus forecasts look for US corporate earnings to grow about 10 % over the next year and Australian earnings to rise around 1 %. While US earnings expectations have been revised down, the downgrades are not unusually large. In Australia, profit expectations have been improving after a rough patch. The biggest risks to profits are that tariffs dent demand and margins in the US and that consumer spending remains weak at home.

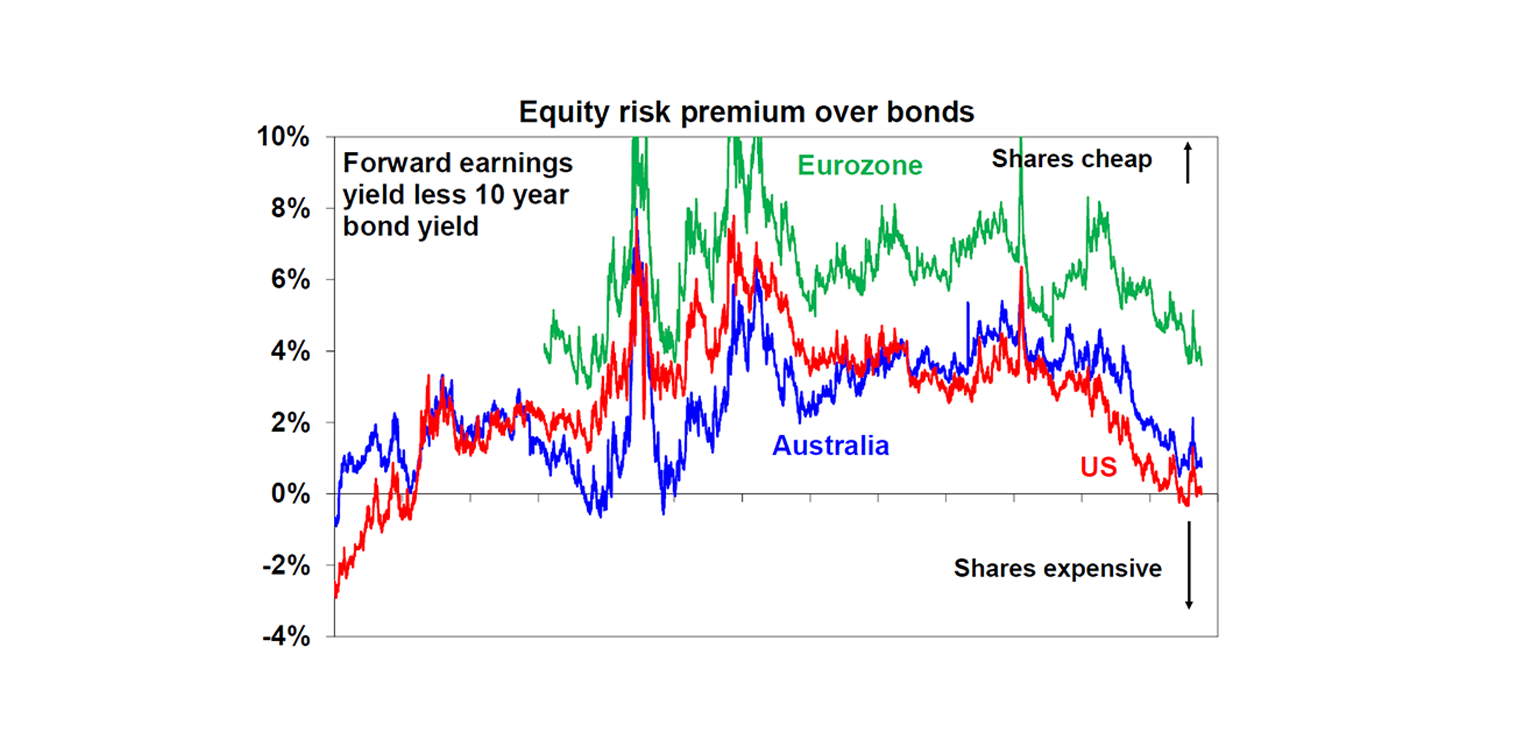

6. The gap between earnings yields and bond yields

Valuation alone doesn’t predict short‑term market moves, but it does indicate the market’s vulnerability. Since 2020, higher bond yields and elevated price‑earnings multiples have squeezed the equity risk premium down to around zero in the US and only a bit higher in Australia. Dr Oliver warns that this leaves share markets susceptible to bad news; cheaper opportunities currently exist in Europe and China. Ideally, lower bond yields and stronger earnings growth would rebuild the buffer.

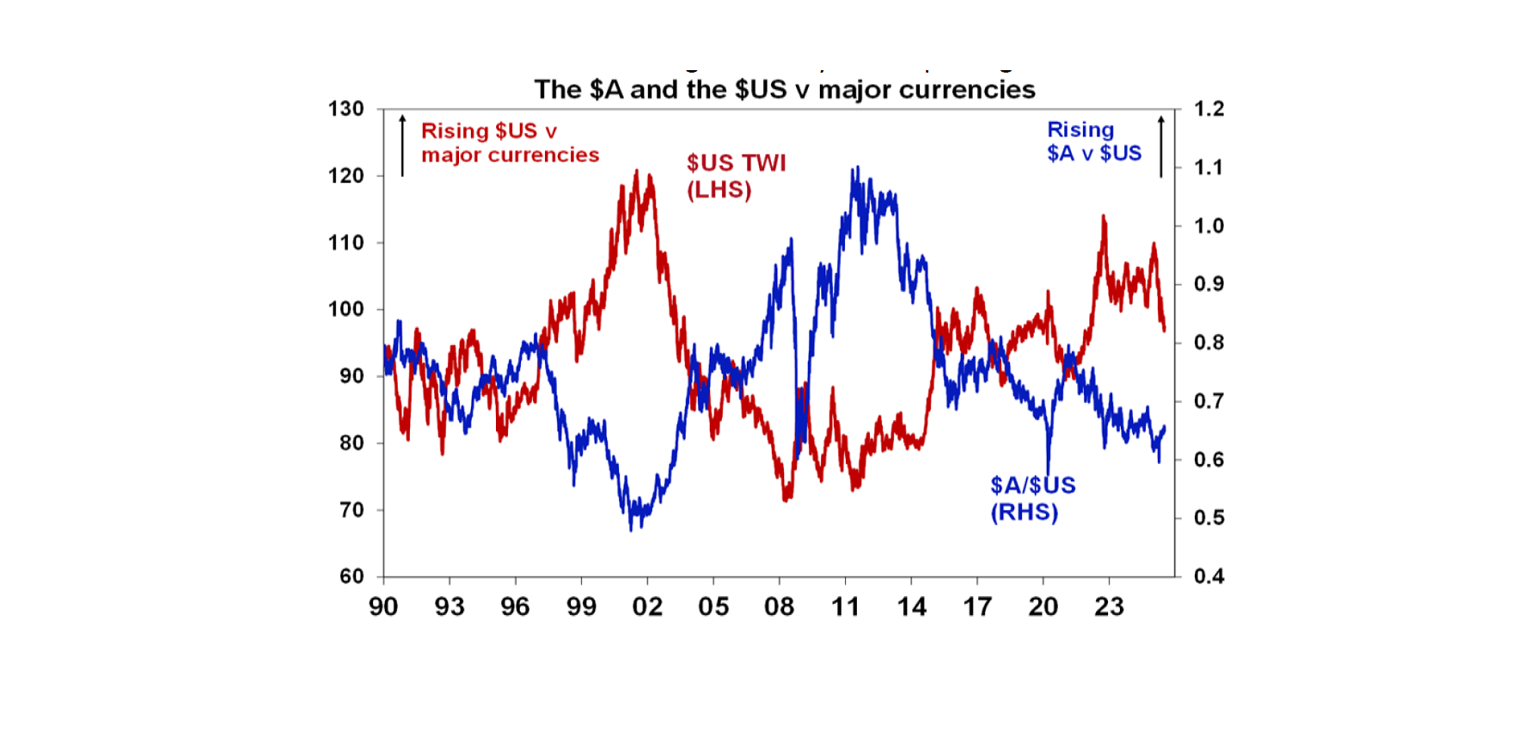

7. The $US matters more than you think

Typically, the US dollar strengthens in times of uncertainty as investors seek safety. But this year the $US has been weak as erratic trade policies have unnerved investors. Dr Oliver notes that the currency is technically oversold and could rebound, which would push the Australian dollar lower. Conversely, if the US dollar continues to drop, it could heighten the risk of a US fiscal crisis and higher bond yields, adding to market volatility.

Putting it all together

Dr Oliver’s seven charts illustrate that while markets have weathered recent shocks, risks remain. Tariffs and recession fears could trigger corrections, inflation expectations may disrupt rate cuts, company profits face headwinds and valuations are stretched. Yet business conditions are holding up, inflation is moderating and policy makers are likely to respond as needed. For investors, the takeaway is to stay diversified, be alert to the indicators above and resist the urge to make hasty decisions based on short‑term noise.

This article has been adapted by I‑Think Financial Group from an insight originally published by AMP. The original commentary and charts are the work of Dr Shane Oliver.