China’s economy sits at the heart of global growth and Australia’s fortunes, so it’s little wonder investors watch Beijing’s moves closely. Dr Shane Oliver, AMP’s Chief Economist, recently unpacked the near‑term risks from US tariffs alongside longer‑term structural issues facing China. We’ve distilled his analysis into five themes and added context on why it matters for Australian investors.

1. Growth has slowed but remains resilient

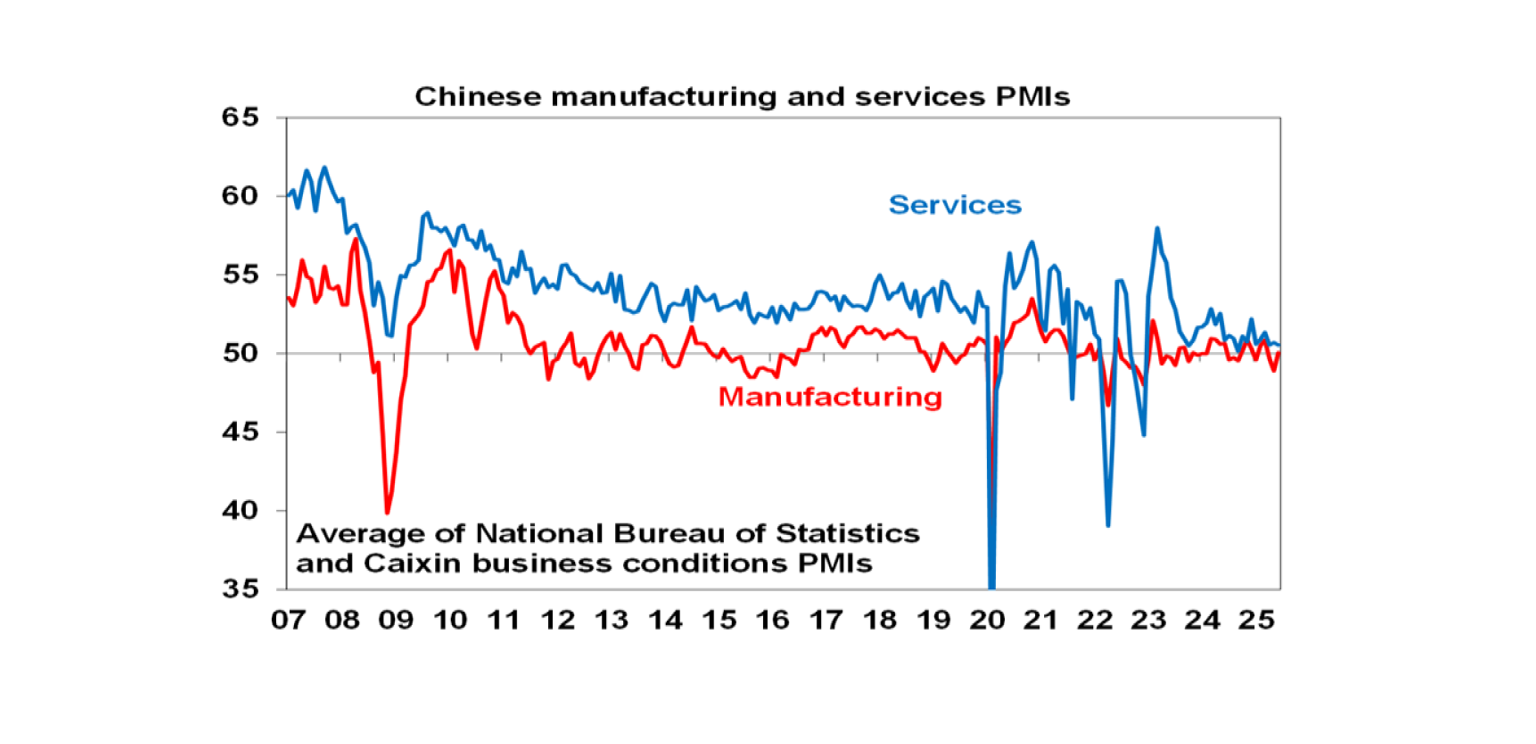

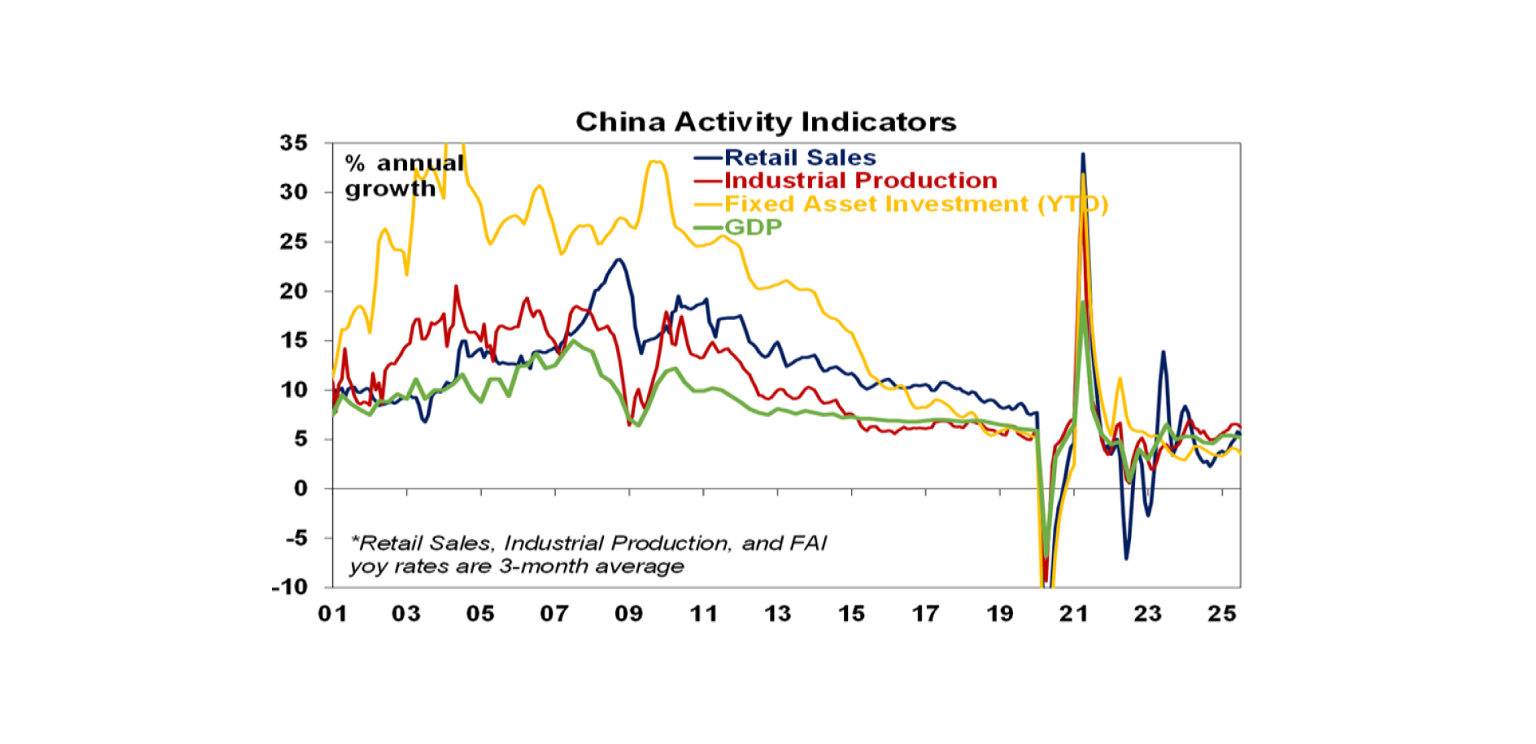

China’s growth rate has eased from double‑digit highs to around 5 % in recent years, but it remains solid by developed‑world standards. Manufacturing surveys and an activity indicator covering industrial production, retail sales and exports suggest momentum is soft but not collapsing. Policy support and growing exports outside the US are helping cushion the drag from the property slump and tariff uncertainty.

2. Tariff threats and a property slump are the near‑term headwinds

Despite the broader resilience, two cyclical risks loom. On the trade front, renewed US tariff threats could depress confidence and demand, even though China’s exports to other markets have been a bright spot. Meanwhile, China’s property downturn is deepening: investment and prices are falling and construction times have lengthened. Policy makers are expected to provide targeted support, but they are unlikely to unleash the kind of mega‑stimulus seen in past cycles.

3. Six structural challenges could cap long‑term growth

Beyond the immediate tariff and property issues, Dr Oliver highlights six longer‑term headwinds that could slow China’s potential growth to around 3 % in the coming decade:

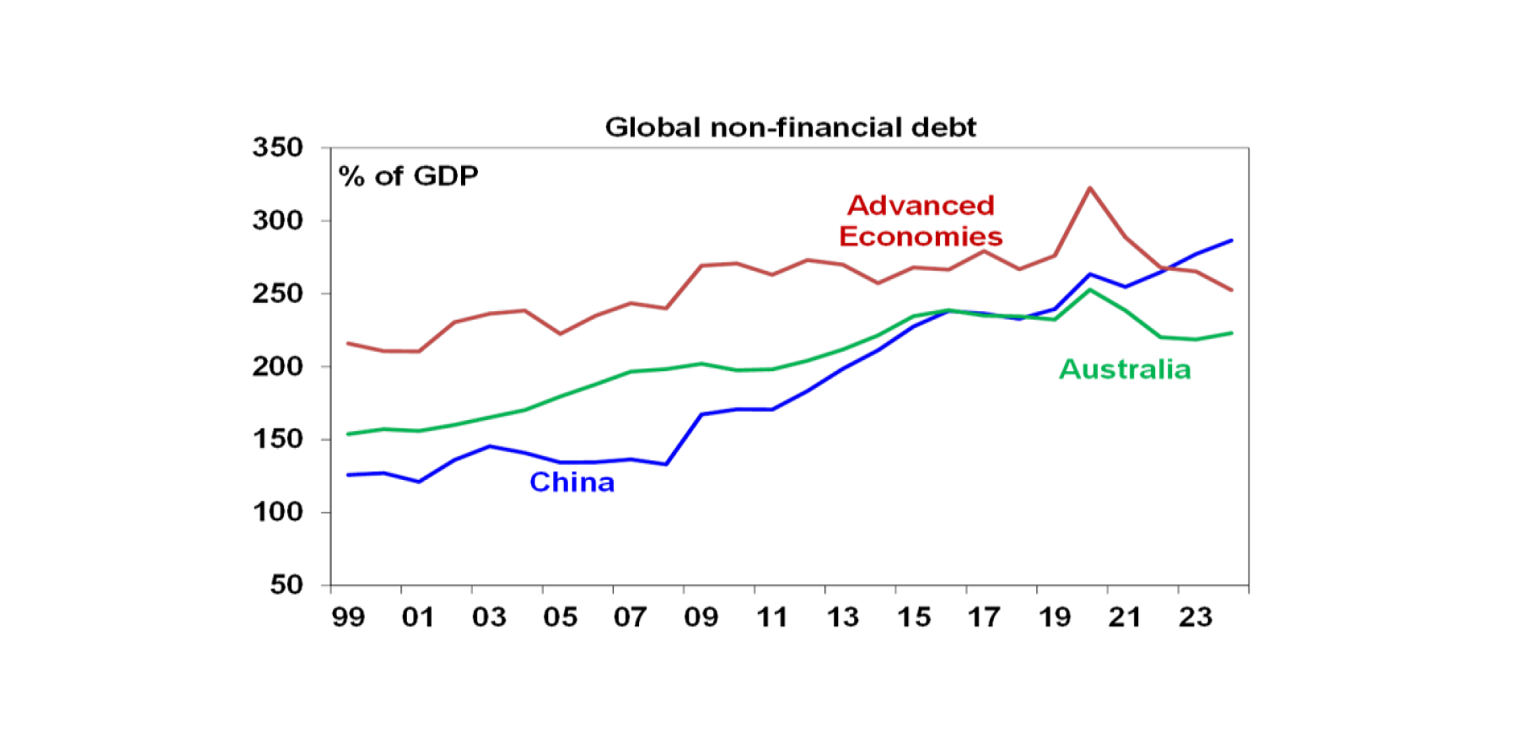

- Excessive savings and debt leading to poor capital allocation and boom‑bust cycles.

- Export‑focused investment faces diminishing returns amid trade restrictions and slowing global demand.

- Property investment is weighed down by oversupply in many cities.

- Demographics are deteriorating as the working‑age population shrinks and the overall population begins to fall.

- State intervention is increasing, risking a so‑called middle‑income trap by crowding out private innovation.

- A fiscal mismatch means local governments bear spending responsibilities without sufficient revenue, fuelling off‑balance‑sheet borrowing.

4. Policy stimulus and green shoots offer some hope

Dr Oliver argues that policy makers will continue to loosen fiscal and monetary settings in an incremental, reactive way – enough to keep growth near 5 % but not enough to re‑ignite a credit boom. There are also a few positive structural developments: generous baby bonuses to counter population decline, signals of support for technology entrepreneurs after years of crackdowns, the global success of Chinese brands, and measures aimed at reducing industrial overcapacity. These steps won’t resolve the structural challenges overnight, but they could mitigate the slowdown.

5. What this means for Australia and investors

Australia’s economy is less sensitive to swings in China than it once was: commodity prices remain robust, population growth is strong and the mining investment cycle is muted. Still, China’s growth path matters for our exports and the outlook for the Australian dollar. Dr Oliver concludes that Chinese growth is likely to trend lower but not collapse, suggesting iron ore prices may stay elevated yet not surge. For investors, that means staying diversified, watching Beijing’s policy moves and recognising that slower growth in China could weigh on global markets but does not herald a downturn.

This article has been adapted by I‑Think Financial Group from an insight originally published by AMP. The original commentary and charts are the work of Dr Shane Oliver.